Project summary

Project summary

Lenkie's underwriting team assess every credit application and decide whether to extend a facility, under what conditions, and at what risk. To underwrite a single deal, an underwriter needed several browser tabs opened simultaneously.

Decisions took too long, details were missed, and when deals were declined the sales team had no visibility into why. A full redesign brought:

* Median decision time to "Yes" from 40 hours to 23 hours,

* Median time to "No" from 42 hours to 17 hours and the

* AI-powered risk report caught a £200,000 lending risk in the pilot.

Lenkie's underwriting team assess every credit application and decide whether to extend a facility, under what conditions, and at what risk. To underwrite a single deal, an underwriter needed several browser tabs opened simultaneously.

Decisions took too long, details were missed, and when deals were declined the sales team had no visibility into why. A full redesign brought:

* Median decision time to "Yes" from 40 hours to 23 hours,

* Median time to "No" from 42 hours to 17 hours and the

* AI-powered risk report caught a £200,000 lending risk in the pilot.

Context

Context

"We need underwriters to see everything they need before they start, work through a consistent process, and arrive at a decision they can defend. Right now, none of those three things are reliably happening."

"We need underwriters to see everything they need before they start, work through a consistent process, and arrive at a decision they can defend. Right now, none of those three things are reliably happening."

Johannes Bouse - Head of Risk at Lenkie

Old underwriting app

Old underwriting app

Problems with the old flow

Problems with the old flow

Decisions required several browser tabs to gather all necessary information

Flat table gave no pipeline visibility across deal stages

Key information scattered across multiple separate views

No structured assessment process or documentation

No error or completeness checking before decisioning

No AI-assisted risk context to support the underwriter

Sales team had no visibility into declined deal rationale

Decisions required several browser tabs to gather all necessary information

Flat table gave no pipeline visibility across deal stages

Key information scattered across multiple separate views

No structured assessment process or documentation

No error or completeness checking before decisioning

No AI-assisted risk context to support the underwriter

Sales team had no visibility into declined deal rationale

Decisions required several browser tabs to gather all necessary information

Flat table gave no pipeline visibility across

deal stagesKey information scattered across multiple separate views

No structured assessment process or documentation

No error or completeness checking before decisioning

No AI-assisted risk context to support the underwriter

Sales team had no visibility into declined

deal rationale

Goals for the redesign

Goals for the redesign

Faster time to yes: good deals approved without unnecessary delay

Faster time to no: weak deals identified and declined quickly

All information visible before assessment begins

A structured, auditable scorecard process

AI-generated risk summary to reduce manual research

A sales review step to close the loop on declined applications

Faster time to yes: good deals approved without unnecessary delay

Faster time to no: weak deals identified and declined quickly

All information visible before assessment begins

A structured, auditable scorecard process

AI-generated risk summary to reduce manual research

A sales review step to close the loop on declined applications

Digging deeper

Digging deeper

I had direct access to the Head of Risk, who owned the process end to end, and the CTO, who sat in the same office as the underwriting team and had observed their working patterns more closely than anyone else on the product side. I supplemented those conversations with informal sessions directly with underwriters.

Key observations:

Underwriters had built their own checklists in spreadsheets to compensate for the tool's gaps

Running notes lived in separate documents outside the system entirely

Each underwriter had personal conventions for which information to check first

None of this seemed structured to the business

I had direct access to the Head of Risk, who owned the process end to end, and the CTO, who sat in the same office as the underwriting team and had observed their working patterns more closely than anyone else on the product side. I supplemented those conversations with informal sessions directly with underwriters.

Key observations:

Underwriters had built their own checklists in spreadsheets to compensate for the tool's gaps

Unassigned deals meant that no one was truly accountable for the deal in the pipeline

Running notes lived in separate documents outside the system entirely

Each underwriter had personal conventions for which information to check first

None of this seemed structured to the business

I had direct access to the Head of Risk, who owned the process end to end, and the CTO, who sat in the same office as the underwriting team and had observed their working patterns more closely than anyone else on the product side. I supplemented those conversations with informal sessions directly with underwriters.

Key observations:

Underwriters had built their own checklists in spreadsheets to compensate for the tool's gaps

Running notes lived in separate documents outside the system entirely

Each underwriter had personal conventions for which information to check first

None of this seemed structured to the business

Pinpointing solutions

Pinpointing solutions

I mapped potential directions into a working reference and used it to anchor further conversations with the team.

After several deliberations on the side of the underwriters as well as the business as a whole, the following solutions arose.

I mapped potential directions into a working reference and used it to anchor further conversations with the team.

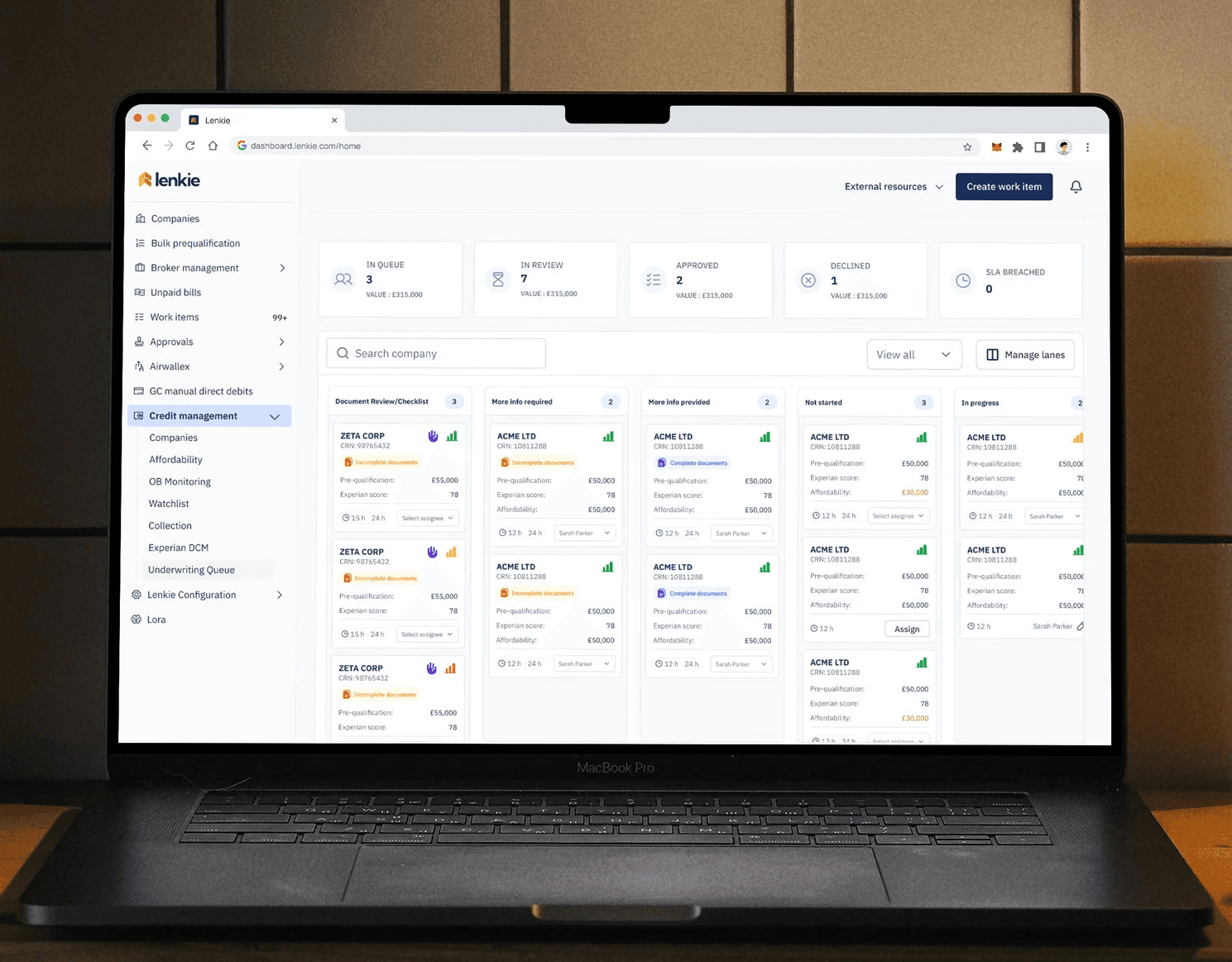

Pipeline swim lanes

Deal cards organised by stage, showing assignee, size, and adverse flags at a glance. Full pipeline visible in seconds.

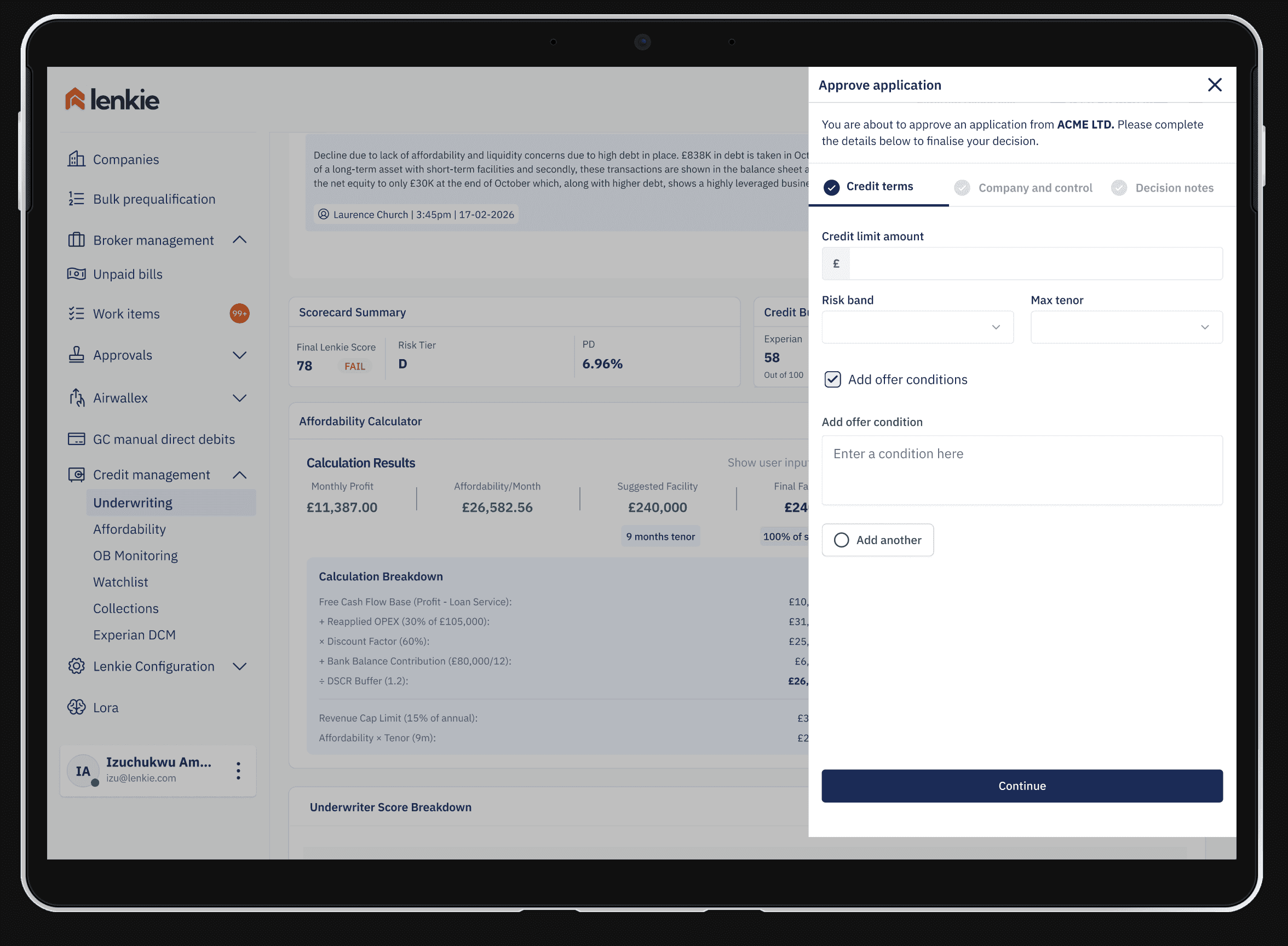

Structured scorecard

A guided workflow across financials, directors, credit history. Underwriters document as they go. Decisioning only unlocks when every section is complete.

Customisable section ordering

Customisable section ordering

Customisable section ordering

Surfaced in feedback: different deals need different sequences. Underwriters reorder scorecard sections by drag-and-drop to match how they think.

Form completeness check

Form completeness check

The tool validates before decisioning is unlocked. Incomplete sections surface visually. No partial assessments reach the decision stage.

AI risk report

Entry point to every deal, not a supplementary view. Adverse media, company structure, and financial signals surface before the scorecard begins.

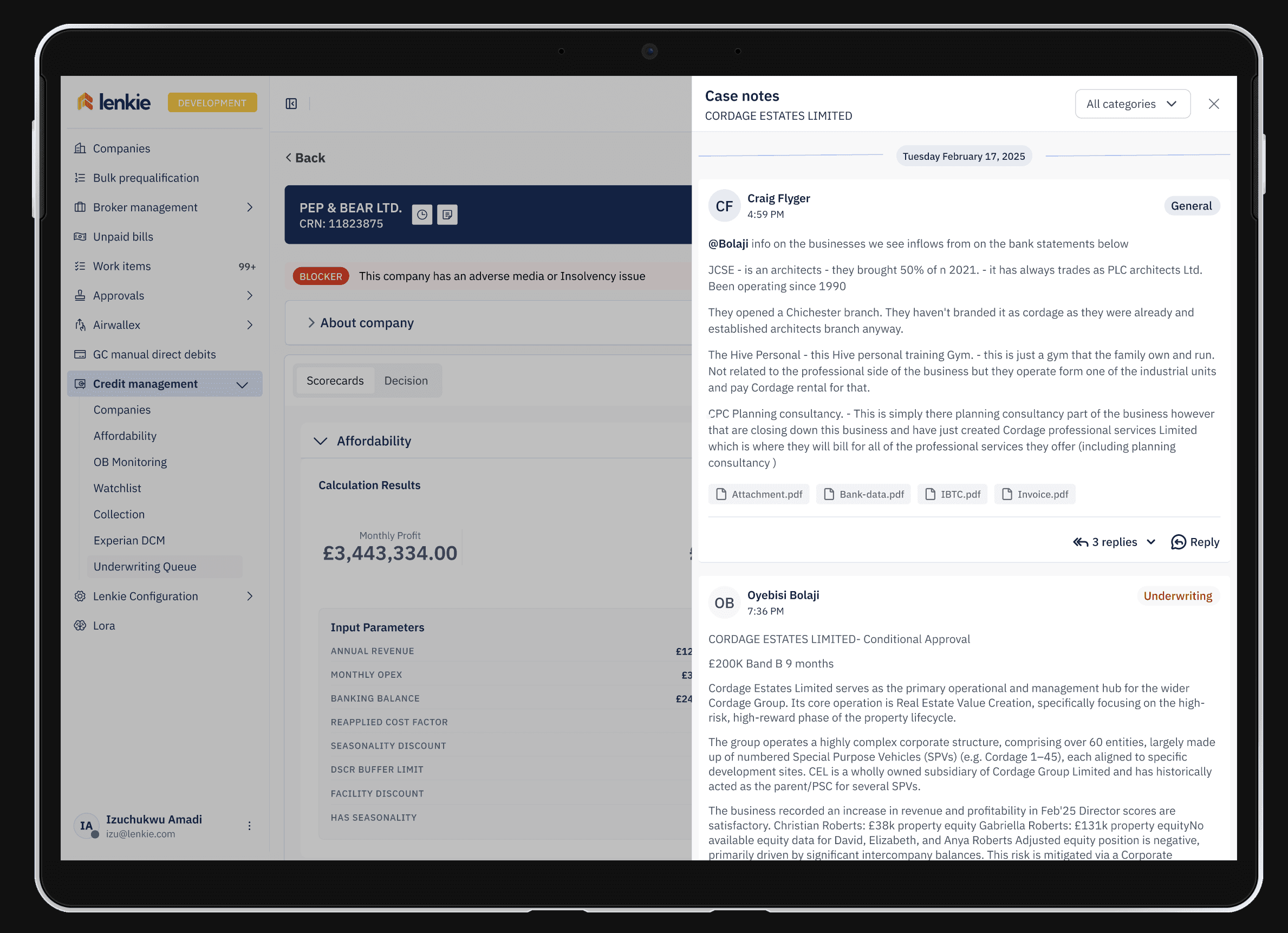

Decision documentation and sales review

Decision documentation and sales review

Underwriters document rationale before finalising. Sales can review declined deals and accept or escalate. A long-standing friction point, resolved.

Bringing the Solution to Life

Bringing the Solution to Life

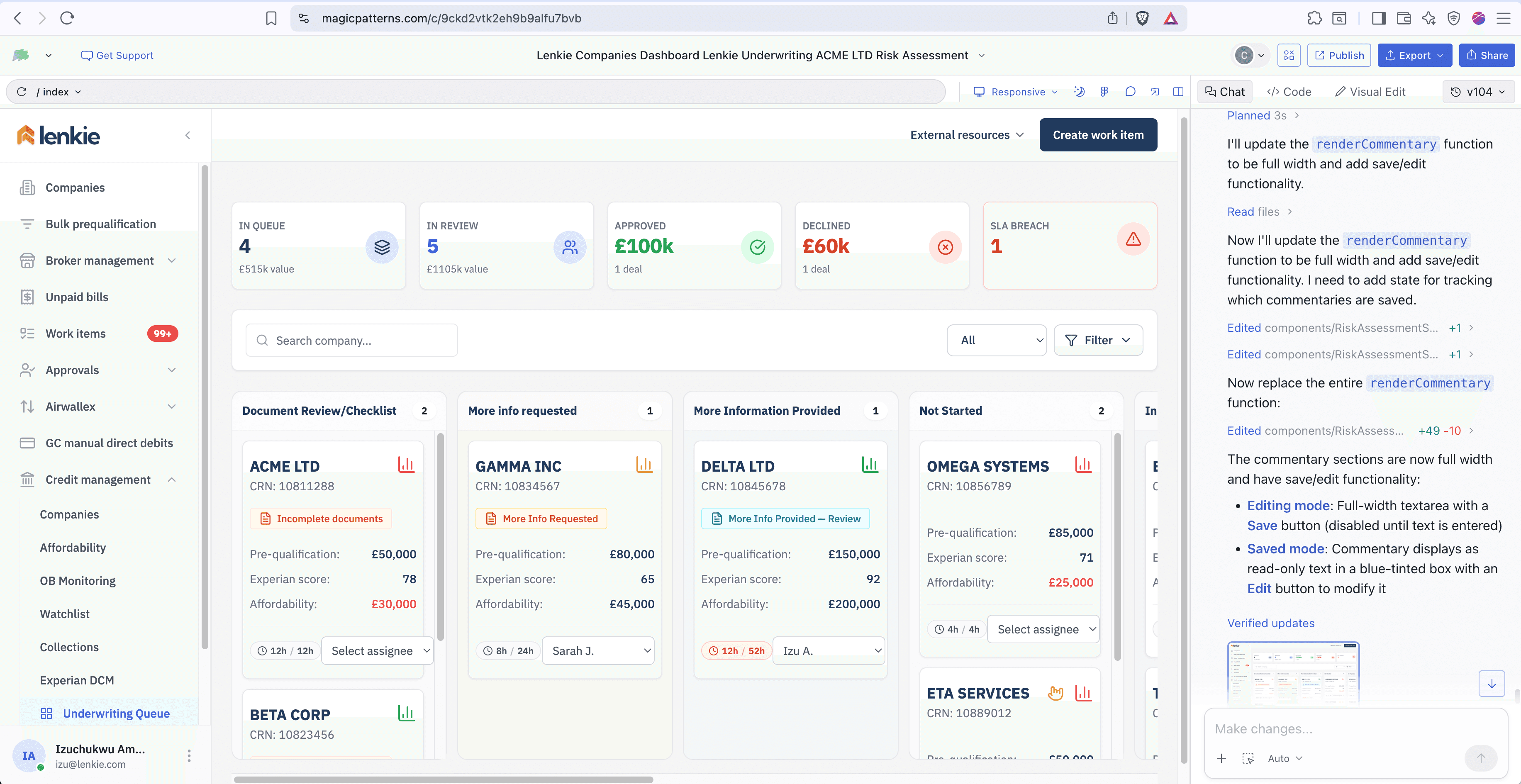

With alignment on direction, I used Magic Patterns to rapidly generate interface concepts, giving the team something tangible to react to early and keeping the design process grounded in real feedback rather than abstract decisions.

With alignment on direction, I used Magic Patterns to rapidly generate interface concepts, giving the team something tangible to react to early and keeping the design process grounded in real feedback rather than abstract decisions.

Screenshot of design in Magicpatterns AI

Screenshot of design in Magicpatterns AI

Design approval

Design approval

As soon as the AI prototypes were approved, I worked closely with my design colleague and also brought him up to speed on what needs to be done. He eventually handled the case notes threading to ensure that all communications on a deal had a single source of truth.

As soon as the AI prototypes were approved, I worked closely with my design colleague and also brought him up to speed on what needs to be done. He eventually handled the case notes threading to ensure that all communications on a deal had a single source of truth.

Validating the Impact

Validating the Impact

The redesigned tool launched in March 2026. The results were concrete, month-on-month measurements, not directional signals.

The redesigned tool launched in March 2026. The results were concrete, month-on-month measurements, not directional signals.

23hrs

23hrs

Median time to "Yes" in March, down from 40 hours in February

Median time to "Yes" in March, down from 40 hours in February

17hrs

17hrs

Median time to "No" in March, down from 42 hours

Median time to "No" in March, down from 42 hours

£200k

£200k

Lending risk identified and avoided by AI adverse media detection

Lending risk identified and avoided by AI adverse media detection

What this project reinforced

What this project reinforced

Internal tools are lower-stakes design work only if you ignore what the tool is actually for. The decisions underwriters make determine which businesses receive funding and how much risk Lenkie carries. The design of the tool is a risk management intervention.

The £200,000 detection was not a coincidence. It was the result of building a tool where critical information was impossible to miss.

Internal tools are lower-stakes design work only if you ignore what the tool is actually for. The decisions underwriters make determine which businesses receive funding and how much risk Lenkie carries. The design of the tool is a risk management intervention.

The £200,000 detection was not a coincidence. It was the result of building a tool where critical information was impossible to miss.

More works

More works

40 hours to 23: Redesigning credit underwriting for faster, more defensible decisions

40 hours to 23: Redesigning credit underwriting for faster, more defensible decisions

ROLE

Lead Designer

TAGS

Product

Mar. 2026

COMPANY

Lenkie Technologies

COLLABORATORS

Remy Dike - Designer

Abiodun Olonu | Paul Emas - Frontend

Kennedy Sigauke | Vincent Nyanga | Nonso Udenwani - Backend